• INSTRUCTIONS ONLY • NO RETURNS •

hio

2022

Instructions for Filing Original and Amended:

• Individual Income Tax (IT 1040)

• School District Income Tax (SD 100)

hio

Department of

Taxation

tax. hio.gov

Net operating loss (IT NOL) ..................50

Nonresident credit (IT NRC) ............23-26

Nonresident statement (IT NRS) ....13, 49

Payment options .....................................6

Refund status .........................................2

Residency ............................................. 11

Resident credit (IT RC) ......................... 26

Residency credits .................................22

Retirement income credit......................20

Schedule of Adjustments .................15-19

Schedule of Credits..........................20-23

School district numbers....................40-45

SD 100

Completing the top portion................13

General information ..........................46

Line instructions ................................ 47

School district tax rates ................ 40-45

Senior citizen credit ........................20, 47

Social Security income .........................16

Use (sales) tax

Instructions........................................14

Worksheet ......................................... 31

Highlights for 2022..................................5

Individual credits .............................. 20-21

Income statements (W-2, 1099) ......38-39

Interest............................................15, 47

IT 1040

Completing the top portion ................13

General information .......................... 11

Line instructions ...........................14-15

Income tax rates and tables ......... 31-37

Joint ling credit ....................................20

Lump sum credits

Instructions........................................20

Worksheets .......................................29

Mailing addresses...................................6

Medical & health care expenses

Instructions........................................18

Worksheet ......................................... 27

Military .........................................9, 17-18

Modied adjusted gross income ............. 7

Amended returns .................................... 8

Business credits ..............................21-23

Business income

Business income deduction (IT BUS) ... 19

Denitions and examples ..................10

College savings (Ohio 529 plan)

Instructions........................................18

Worksheet ......................................... 28

Deceased taxpayers ...............................7

Direct deposit options ............. Back cover

Donations .......................................12, 15

Earned income credit............................21

Electronic ling options ........... Back cover

Estimated tax payments for 2023 ........... 7

Exemptions ...........................................14

Filing extensions ...............................7, 13

Filing requirements ......................... 11, 46

General information ................................ 7

Table of Contents

A

B

C

D

F

G

I

J

L

M

P

S

N

U

R

2022 Ohio IT 1040 / SD 100

Check Your Refund Status Anytime, Anywhere!

¬ 24-Hour Hotline - 1-800-282-1784

¬ Online at tax.ohio.gov/refund

¬ Mobile App - Search "Ohio Taxes" on your device's app store.

E

H

These instructions contain law references for specic line items and requirements. To review Ohio income and school district

income tax law, see codes.ohio.gov/orc/5747 and codes.ohio.gov/orc/5748, respectively.

Federal Privacy Act Notice: Because we require you to provide us with a Social Security number, the Federal Privacy Act of 1974 requires us to inform you that providing us

with your Social Security number is mandatory. Ohio Revised Code sections 5703.05, 5703.057 and 5747.08 authorize us to request this information. We need your Social

Security number in order to administer this tax.

2

Need Help? – To help answer your questions and ensure that your tax returns are led accurately, the Department of Taxation

provides the following resources at tax.ohio.gov:

*Persons who use text telephones (TTYs) or adaptive telephone equipment only: Contact the Ohio Relay Service at 7-1-1 or

1-800-750-0750 and give the communication assistant the Ohio Department of Taxation phone number that you wish to contact.

Additional Resources

Volunteer Income Tax Assistance Program (VITA) and Tax Counseling for the Elderly (TCE): These programs help

persons with disabilities as well as elderly, low-income and limited English-speaking taxpayers complete their state and

federal returns. For locations in your area, call 1-800-906-9887, or visit their website:

http://www.irs.gov/Individuals/Free-Tax-Return-Preparation-for-You-by-Volunteers

AARP: Trained and certied AARP tax aide volunteer counselors assist low- to middle-income taxpayers, with special

attention to those age 50 and older. For more information, call 1-888-227-7669 or visit their website:

http://www.aarp.org/money/taxes/aarp_taxaide/

Taxpayer Assistance

2022 Ohio IT 1040 / SD 100

Forms – Find all individual and school district income tax forms (including related schedules and worksheets). Many forms have

ll-in versions that you can complete online, print, and then submit to the Department. You can also request tax forms anytime

by calling 1-800-282-1782.

FAQs – Review answers to common questions on topics such as business income and residency issues.

Online Services – File your state and school district income tax returns for free. There are also several self-service options

such as making payments, viewing transcripts, and accessing your 1099-G and 1099-INT statements from the Department.

Online Notice Response Service – Securely submit documents online in response to most notices or requests for ad-

ditional information sent by the Department.

Guest Payment Service – Make individual and school district income tax payments electronically without having to register

for an Online Services account.

Information Releases – Research detailed explanations and legal analyses of certain tax topics such as residency and tax

issues facing military servicemembers and their civilian spouses.

The Finder – Look up your address to determine if you live in a taxing school district as well as the tax rate and four-digit

school district number.

Ohio Virtual Tax Academy – View webinars designed and presented by Department sta on Ohio's state taxes.

Tax Alerts – Sign up to receive tax updates and reminders from the Department via email.

Email – Visit tax.ohio.gov/emailus to access a

secure email form. Complete all required elds

before submitting your question.

Call – You may call to speak with an examiner

at 1-800-282-1780* during the Department's

normal business hours (8:00 a.m. to 5:00 p.m.,

Monday through Friday excluding holidays).

Write – Contact the Department by mail at:

Ohio Department of Taxation

P.O. Box 182847

Columbus, OH 43218-2847

3

Contact Us - If you cannot nd the answer using the website, you may contact the Department using any of the following

methods:

A Message From the Ohio Tax Commissioner

Dear Ohio Taxpayers,

Thank you to all Ohioans for taking the time to prepare and le the 2022 Ohio income tax return.

You will nd some changes this year to Ohio’s income tax ling system. This instruction booklet will explain those changes and

how best to ll out your return.

Please note some of the changes to Ohio’s income tax for tax year 2022:

• All tax brackets have been adjusted for ination. As a result, taxpayers with taxable income of $26,050 or less will pay no

income tax.

• A new addition and credit are applicable to investors in a pass-through entity that les the IT 4738.

• A new, nonrefundable credit is available for employing certain persons enrolled in a certied vocational training program.

If you aren’t already ling your tax return electronically, please consider joining the 93 percent of taxpayers who do so. It’s more

accurate, more secure, and the quickest way to get a refund. Remember, you can le your Ohio tax return online and for free

with our I-File system.

Please keep in mind the deadline for ling both your Ohio and federal tax return is April 18, 2023. And as a reminder, a request

for a ling extension does not extend your payment due date.

If you have any questions or need assistance with your return, you can contact our Taxpayer Assistance line at 1-800-282-

1780, or click on ‘Contact Us’ at tax.ohio.gov.

Best wishes,

Je McClain

Ohio Tax Commissioner

Our Mission

To provide quality service to Ohio taxpayers by helping them comply with their tax responsibilities and by fairly applying the tax law.

2022 Ohio IT 1040 / SD 100

IMPORTANT: The printed version of these instructions are accurate as of December 12, 2022. The following corrections have been made

to the online version:

• Page 17: "Space Force" was added to the list of uniformed services in the line 28 instruction.

4

Ohio Income Tax Tables. For tax year 2022, individuals with

Ohio taxable nonbusiness income of $26,050 or less are not subject

to Ohio income tax. Also, the tax brackets have been indexed for

ination per Ohio Revised Code section 5747.02(A)(5). See pages

31-37.

Pass-Through Entity Related Addition and Credit. A new

addition and credit are applicable to investors in a pass-through

entity that les the IT 4738. See pages 15 and 23.

Vocational Job Credit. A new nonrefundable credit is

available for individuals who employ eligible employees in a work

based learning experience, internship, or cooperative education

program and were issued a credit certificate from the Ohio

Department of Education. See the instructions on page 21.

Guest Payment Service. The Department now has an option to

make Ohio income tax payments without registering for an account.

For more information, see tax.ohio.gov/Pay.

Schedules of Withholding. Paper filers must complete the

Schedule of Ohio Withholding (and Schedule of School District

Withholding) listing each income statement reporting Ohio (or school

district) tax withheld. See pages 14 and 47 for more information.

Beginning with tax year 2019,

your exemption amount, certain credits, and the school district

income tax bases are determined using "modied adjusted gross

income" or "modied adjusted gross income less exemptions." See

the instructions on page 7.

Electronic Estimated Payments. Estimated payments can be

submitted with your electronically led Ohio IT 1040 and/or SD

100 through a participating third-party tax preparation product.

Payments may be future-dated but must be scheduled by the 4th

quarter estimated payment due date.

Electronic 1099-G. Your 1099-G is available to view and print using

Online Services at tax.ohio.gov/File. You can elect to receive your

1099-G electronically.

Highlights for 2022

2022 Ohio IT 1040 / SD 100

Write legibly using black ink and UPPERCASE letters.

Double-check your demographic information.

• Verify your name(s) and SSN(s) are correct.

• Verify your current address. If you are due a refund, it will be

mailed to this address.

Verify the forms and vouchers are for the correct tax year.

• The Department releases new forms and vouchers each tax

year. Do not change the year on the form or voucher. If you

do this, processing of your form or voucher may be delayed.

Do not write on software-generated returns.

• If you print a software-generated return from a tax preparation

program and later need to change information on the return,

do not write in the changes. Use the software to make the

necessary changes and reprint the return.

• The Department’s system will not pick up handwritten changes

on returns generated by tax preparation software.

Use the proper payment voucher.

• Use the Ohio IT 40P to pay your Ohio income tax, and the

Ohio SD 40P to pay your school district tax due.

• If you are amending your return(s), use the Ohio IT 40XP to

pay your Ohio income tax, and the Ohio SD 40XP to pay your

school district tax due.

Do not staple, paper clip, or otherwise attach your return

together.

• This will allow the Department to process your return as

quickly as possible. We will ensure your return information

stays grouped together.

● To round, drop any cents less than 50 cents and increase

amounts 50 cents or above to the next dollar.

Include all necessary schedules and worksheets.

• If you have an amount on line 2a and/or 2b of your IT 1040,

include the Ohio Schedule of Adjustments.

• If you have an amount on line 9 and/or 16 of your IT 1040,

include the Ohio Schedule of Credits and any appropriate

worksheets.

• If you have an amount on line 11 of your Ohio Schedule of

Adjustments, include the Ohio Schedule IT BUS.

• If you have dependents, include Ohio Schedule of Dependents.

• Ensure your return is placed in the proper order:

1) Ohio IT 1040 (pages 1 and 2)

2) Ohio Schedule of Adjustments

3) Ohio Schedule IT BUS

4) Ohio Schedule of Credits

5) Ohio Schedule of Dependents

6) Ohio Schedule of Withholding

7) Worksheets and attachments

8) Wage and income statements

• If you have an amount on line 14 of your IT 1040 and/or an

amount on line 7 of your SD 100, include the Schedule of Ohio

Withholding and/or Schedule of School District Withholding

as well as copies of your wage and income statements.

• If you are claiming any refundable and/or nonrefundable busi-

ness credits on your Ohio Schedule of Credits, include copies

of the required certicates and/or Ohio K-1s.

Do not include any banking information with your return.

• Direct deposit of individual income and school district income

tax refunds is not available to paper lers.

send each return in its own envelope.

Common Filing Tips for Paper Filers

5

ACI Payments charges a service fee of 2.65%

of your payment or $1, whichever is greater.

Ohio does not receive any of this fee.

The payment will appear on your credit card

statement as two separate entries – one for

the payment and another for the service fee.

What information do I need when using

this payment method?

Please have the following information

available:

● The Ohio jurisdiction code: 6446;

● Your SSN and your spouse’s SSN (if l-

ing jointly);

● The tax year of your payment;

● The payment amount;

● Your credit or debit card number and

expiration date; AND

● The school district number (if making a

school district income tax payment).

How do I make a debit or credit card

payment by phone?

When you call ACI Payments:

● First, when prompted, enter “2”.

● Second, when prompted, enter “6446#”.

● Third, verify the information. If correct,

enter “1”.

● Fourth, when prompted, enter “1” if ma-

king an income tax payment, or “2” if

making a school district income tax

payment.

You will then be prompted to enter your

payment information.

Generally, Ohio income and school district

income tax is due by April 18, 2023. There

are several options for paying these taxes.

Payments for Ohio and school district

income taxes must be made separately.

The Department is not authorized to

set up payment plans. You may submit

partial payments toward any outstanding

tax, interest, or penalty. However, such

payments will not stop the Department's

billing process or collection attempts by the

Ohio Attorney General's Oce.

Electronic Check

Any ler can pay by electronic check via

the Department's Online Services or Guest

Payment service, both available at tax.ohio.

gov/Pay.

Note: If you are ling in Ohio for the rst

time, you may not be eligible to use the

Department's Online Services or Guest

Payment service to pay your Ohio income

taxes.

Additionally, electronic lers can follow their

ling software's payment prompts at the time

they le their returns.

An electronic check withdraws funds directly

from your checking or savings account.

There is no fee for using this payment

method. Generally, your payment will be

withdrawn within 24 hours of the date you

choose for payment. You must ensure that

the funds are in your account and available

on the date you choose for payment. The

payment will show on your bank statement

as “STATE OF OHIO”.

You can delay payment until the payment

deadline of April 18, 2023. You can also pay

your quarterly 2023 Ohio individual and/or

school district estimated income tax with

this method.

Important: Future-dated payments can

only be modied through the Department's

Online Services at tax.ohio.gov/File.

Debit or Credit Card

Any ler can pay using a debit or credit card

(Discover, Visa, MasterCard, or American

Express). These payments can be made

via tax.ohio.gov/Pay or www.acipayon-

line.com. You can also pay over the phone

by calling 1-800-272-9829. You cannot

future-date a debit or credit card payment.

Note: ACI Payments, Inc. processes all

debit and credit card payments.

Payment Options and Mailing Addresses

2022 Ohio IT 1040 / SD 100

What if there’s a problem with my

payment?

Call ACI Payments at 1-800-487-4567.

Paper Check or Money Order

Any ler can pay by check or money order.

If you use a money order, keep a copy for

your records. You will be charged a $50 fee

for writing a bad check.

Ohio IT 1040: Make your check or money

order payable to “Ohio Treasurer of State.”

Include the tax year, form name, and

the last four digits of your SSN on the

“Memo” line. Include the appropriate

voucher:

● IT 40P for original returns; OR

● IT 40XP for amended returns.

SD 100: Make your check or money order

payable to “School District Income Tax.”

Include the tax year, form name, the last

four digits of your SSN, and the school

district number on the "Memo" line.

Include the appropriate voucher:

● SD 40P for original returns; OR

● SD 40XP for amended returns.

All payment vouchers are available at tax.

ohio.gov/forms.

6

Where Should I Mail My Return and/or Payment?

Mail To:

Ohio Department of Taxation

P.O. Box 2679

Columbus, OH 43270-2679

Ohio Department of Taxation

P.O. Box 2057

Columbus, OH 43270-2057

Ohio Department of Taxation

P.O. Box 182197

Columbus, OH 43218-2197

Ohio Department of Taxation

P.O. Box 182389

Columbus, OH 43218-2389

Mail To:

Ohio Department of Taxation

P.O. Box 182131

Columbus, OH 43218-2131

Ohio Department of Taxation

P.O. Box 182389

Columbus, OH 43218-2389

If Submitting Ohio Form:

IT 1040 without payment

IT 1040 with payment (include Ohio IT 40P / IT 40XP)

SD 100 without payment

SD 100 with payment (include SD 40P / SD 40XP)

If Only Submitting Payment With Voucher:

IT 40P / IT 40XP

SD 40P / SD 40XP

General Information for the Ohio IT 1040 and SD 100

1st quarter - April 18, 2023

2nd quarter - June 15, 2023

3rd quarter - Sept. 15, 2023

4th quarter - Jan. 16, 2024

2022 Ohio IT 1040 / SD 100

When Are My Ohio Returns Due?

Most taxpayers must le their Ohio IT 1040

and SD 100 (if applicable) by April 18, 2023.

You must le your return by this date even

if you are unable to pay the tax due. For an

exception for certain military servicemem-

bers, see page 9.

Filing extensions: Ohio does not have an

extension request form, but honors the IRS

extension. If you led an IRS extension, your

due date for ling your Ohio IT 1040 and SD

100 is October 16, 2023. Include a copy of

your IRS extension or IRS acknowledgment,

and/or your extension conrmation number.

-

tend the time for payment of the tax due.

You must make extension payments by April

18, 2023 on the Ohio IT 40P and/or SD 40P.

Interest will accrue on any tax not paid by

April 18, 2023, and penalties may also apply.

See R.C. 5747.08(G) and Ohio Adm. Code

5703-7-05.

What Tax Records Do I Need to Keep?

Keep a copy of your:

● Income tax returns and schedules;

● Wage and income statements;

● Supporting documentation;

● Payment records;

for at least four years from the later of the

ling due date or the date you led the re-

turn. You must be able to support all items

listed on your return. See R.C. 5747.17.

How Should I Complete My Income Tax

Returns?

● Only use black ink.

● Round numbers to the nearest dollar.

● Print numbers and letters (UPPER

CASE only) inside the boxes as shown:

A N RTSY E TE1 2 3

When Will I Receive my Refund?

Most taxpayers who file their returns

electronically and request direct deposit

will receive their refunds in approximately

15 business days. Paper returns will take

approximately 8 to 10 weeks to process.

What Information Must a Preparer

Provide?

A tax return preparer must provide his/her

printed name and Preparer Tax Identica-

tion Number (PTIN) on all returns. The

PTIN serves as the preparer's signature.

The preparer should not otherwise sign

the return.

See R.C. 5703.263(C) and 5747.08(F).

Can My Tax Preparer Contact the

Department About My Tax Return?

You may check the box above your tax

preparer's name on page 2 of the return to

authorize your preparer to:

● Contact the Department about the status

of your return, payments, or refund;

● Provide the Department with information

missing from your return; AND

● Respond to inquiries or notices from the

Department related to the return.

You may also complete form TBOR 1, Dec-

laration of Tax Representative available at

tax.ohio.gov/forms. This form authorizes

a tax representative to represent you in any

matter before the Department.

See R.C. 5747.08(J).

Should I Make Estimated Tax Payments

for Tax Year 2023?

If your income is subject to Ohio withholding,

you generally do not need to make estimated

payments. You should make estimated pay-

ments for tax year 2023 if your estimated

Ohio tax liability (total tax minus total credits)

less Ohio withholding is more than $500.

Estimated payments are made quarterly ac-

cording to the following schedule:

Use the Ohio IT 1040ES vouchers to make

estimated Ohio income tax payments. Use

the Ohio SD 100ES vouchers to make es-

timated Ohio school district tax payments.

You can determine your estimated pay-

ments using the worksheet included with the

vouchers. Joint lers should determine their

combined estimated Ohio tax liability and

make joint estimated payments.

Note: Instead of making estimated pay-

ments, you can increase your Ohio with-

holding by ling a revised Ohio IT 4 with

your employer. Also, special rules regarding

estimated payments apply to certain taxpay-

ers with farming and/or shing income. See

Adm. Code 5703-7-04.

If you do not make the required estimated

payments, you may be subject to an interest

penalty for underpayment of estimated taxes.

See form IT/SD 2210.

For more information, see the "Income - Es-

timated Income/School District Taxes and

the 2210 Interest Penalty" topic at tax.ohio.

gov/FAQ.

See also R.C. 5747.09.

What Is Modied Adjusted Gross Income?

Modied adjusted gross income is your Ohio

adjusted gross income (Ohio IT 1040, line 3)

plus your business income deduction (Ohio

Schedule of Adjustments, line 11). If you did

not take a business income deduction, your

modied adjusted gross income matches

your Ohio adjusted gross income.

You will need to know your modied adjusted

gross income to determine your personal

exemption amount and if you qualify for any

of the following credits:

● Retirement income credit;

● Lump sum retirement credit;

● Senior citizen credit;

● Lump sum distribution credit;

● Child care and dependent care credit;

● Exemption credit; AND

● Joint ling credit.

Additionally, if you live in an earned income

tax base school district, your taxable income

is limited to only earned income included in

your modied adjusted gross income.

Use the worksheet on page 31 to calculate

your modied adjusted gross income.

See R.C. 5747.01(II).

What if a Taxpayer Is Deceased?

The taxpayer's representative, such as an

executor or administrator, must le the de-

ceased taxpayer's return by:

● Checking the "Deceased" box after the

applicable SSN;

● Selecting the ling status from the federal

income tax return; AND

● Signing the return on behalf of the de-

ceased.

If the taxpayer is due a refund, the check

will be issued in the taxpayer's name. The

taxpayer's representative can present proof

that she or he is the executor or administrator

to the bank when cashing the check.

If the taxpayer's representative needs the

check reissued to include his or her name,

see the "Income - General" topic at tax.

ohio.gov/FAQ for instructions.

See R.C. 5747.08(A).

What if I Move After Filing My Return?

If you move after ling your return, notify the

Department of your new address as soon

as possible. You should also notify the post

oce at moversguide.usps.com.

7

2022 Ohio IT 1040 / SD 100

Amending Your Ohio IT 1040 and SD 100

!

CAUTION

You can le an amended Ohio IT 1040 or

SD 100 to report changes to your originally

led return(s). An amended return can re-

sult in either a tax due or a refund based on

the changes. Under certain circumstances,

an amended return may be required.

To amend the Ohio IT 1040 or SD 100,

you should le a new return, reecting all

proposed changes, and indicate that it is

amended by checking the box at the top

of page 1. You must include the IT RE with

your amended IT 1040 and/or the SD RE

with your amended SD 100. Use your cur-

rent mailing address on the amended re-

turn. Allow at least 120 days from the date

of receipt to process your amended return.

For more information, see the "Income -

Amended Returns" topic at tax.ohio.gov/

FAQ.

When Not to Amend Your Return

Some common mistakes may not require an

amended return. Some examples include:

● Math errors;

● Missing pages or schedules;

● Demographic errors;

● Missing income statements (W-2, 1099,

K-1) or credit certicates;

● Unclaimed payments or withholding.

In these situations, the Department will ei-

ther make the corrections or contact you to

request documentation.

Requesting a Refund

You may amend your return to request an

additional credit, deduction or payment. Such

changes may result in a refund. Generally,

you have four years from the date of the

payment to request a refund. You must in-

clude documentation to support the changes

reported on your amended return. Some

common required documentation includes:

● Business Income: Page 1 of your federal

return, the federal schedules reporting

your business income, and IT K-1 forms;

● Social security, disability, survivorship, and

retirement benets: Copies of 1099(s),

page 1 of your federal return, and the

retirement plan paying the benets;

● Residency status: Any document sup-

port

ing your residency change including

property records (mortgage statements,

lease agreements, etc.), driver's licenses

or state IDs, voter registration, resident

state tax returns, armed services records

and utility bills.

● Payments/credits: Copies of your income

statements (W-2, 1099, etc.), Ohio IT K-1,

or credit certicates;

● Nonresident credit: Ohio form IT NRC.

See R.C. 5747.11.

Reporting Additional Tax Due

You should amend your return to report addi-

tional income, or reduce a previously claimed

credit or deduction. Such changes may result

in additional tax due. Include payment with

your amended return using an IT 40XP and/

or SD 40XP payment voucher.

Changes to Your Federal Return

If the IRS makes changes to your federal re-

turn, either based on an audit or an amended

return, and those changes aect your Ohio

return(s), you are required to le an amended

IT 1040 and/or SD 100. The IRS noties the

Department of these changes.

Do not le your amended Ohio return(s)

until the IRS has nalized the changes to

your federal return. Once they are nalized,

include a copy of all of the following:

● Your federal 1040X;

● The IRS acceptance letter; AND

● The refund check issued to you by the

IRS, if applicable.

Note: Instead of providing these documents,

you may be able to submit a copy of the

IRS Tax Account Transcript reecting your

updated federal return information.

If there is a change in your ling status and/

or dependents, it must be reected on your

amended Ohio return(s). Additionally, for

changes to dependents, complete an up-

dated Ohio Schedule of Dependents.

Net Operating Loss: To claim a federal NOL

carryback, check both boxes at the top of

the return(s) and include a completed Ohio

Schedule IT NOL. See the instructions for the

Ohio Schedule IT NOL on page 50.

Your amended Ohio IT 1040

no later than 90 days after the

IRS completes its review of

your federal return, even after

the four-year period has passed. Failure

may result in an assessment or a denial

of your refund claim.

See R.C. 5747.10.

Changes to Your Resident Credit

You must le an Ohio amended return based

on changes made by another state if all of

the following are true:

● You claimed a resident credit on your Ohio

IT 1040;

● You led income tax returns in other states;

● The Ohio resident credit claimed was

based on either the taxes due or the taxes

paid to the other states;

● The other states made changes to the

returns; AND

● The changes will aect your Ohio resident

credit calculation.

Your income taxes paid to other states

may change after the four-year period has

passed. If the taxes paid would otherwise

qualify for the Ohio resident credit, you have

an additional 90 days after the changes

have been nalized by the state(s) to le an

amended return and request any refund that

results from the changes.

Once the changes are nalized, please in-

clude a copy of all of the following:

● A revised Ohio form IT RC;

● The other state return(s) or correction

notice(s); AND

● Proof of payment to the other state(s).

See R.C. 5747.05(B)(3).

8

Ohio Income Tax for Military Servicemembers and Their Civilian Spouses

Taxability of a Military Servicemember's Income in Ohio

Taxability of a Servicemember's Civilian Spouse's Income in Ohio

1)

If the spouse is a:

And the spouse and

servicemember:

And the income is

earned:

Then the income is:

Resident of Ohio Nonresident of Ohio

N/A (Skip to #3)

The same state of legal residence Dierent states of legal residence

In Ohio

Taxed in

Ohio

Outside of Ohio

Eligible for the

Resident Credit

In Ohio

Outside of Ohio In Ohio Outside of Ohio

Deductible on

Sch. of Adj.,

line 27

Eligible for the

Nonresident

Credit

Taxed in Ohio

Eligible for the

Nonresident Credit

2)

3)

4)

For more information, see tax.ohio.gov/military, or Information Release IT 2008-02, "Ohio Taxable Income and Deductions for Service-

members and Civilian Spouses." You can also email the Department at [email protected].

1)

If the servicemember

is a:

And the income is

earned:

And the source of

the income is:

Then the income is:

Resident of Ohio

Nonresident of Ohio

Taxed in

Ohio

Deductible on

Sch. of Adj.,

line 27

Taxed in

Ohio

Deductible on

Sch. of Adj.,

line 27

Eligible for the

Nonresident

Credit

2)

3)

4)

In Ohio Outside of Ohio

Military

Service

Non-

Military

Taxed in

Ohio

Deductible on

Sch. of Adj.,

line 26

Eligible for

the Resident

Credit

Military

Service

Non-

Military

Military

Service

Non-

Military

Military

Service

Non-

Military

In Ohio Outside of Ohio

2022 Ohio IT 1040 / SD 100

Residency. A military servicemember is a

resident of their "state of legal residence."

This is generally the same as the service-

member's "home of record" unless it is sub-

sequently changed. The servicemember's

state of legal residence does not change

based on military orders.

A servicemember's civilian spouse will also

retain their original state of legal residence

if the servicemember and spouse have

the same state of legal residence and the

spouse is accompanying the servicemem-

ber as part of military orders. Additionally, a

civilian spouse can elect to have the same

state of legal residence as the servicemem-

ber.

Deductions. Ohio provides ve deductions

to military servicemembers. Only income

included in the taxpayer's federal adjusted

gross income is eligible for these deduc-

tions. For example, Ohio Veterans Bonus

payments are not included in federal adjust-

ed gross income and thus are not deduct-

ible. The following deductions are in the

"Uniformed Services" section of the Ohio

Schedule of Adjustments:

● Line 26 - Deduction for military pay and

allowances for certain active duty service-

members stationed outside Ohio

● Line 27 - Deduction for military pay

earned by a nonresident servicemember

● Line 28 - Deduction for uniformed services

retirement income

● Line 29 - Deduction for military injury relief

fund grants and veteran's disability sever-

ance payments

● Line 30 - Deduction for certain reimburse-

ments and benets received for service in

the Ohio National Guard

Additionally, a servicemember's nonresi-

dent civilian spouse can deduct, on line 27,

compensation earned in Ohio, when the

servicemember and spouse have the same

state of residence and are present in Ohio

due to military orders.

See pages 17-18 for specic instructions on

each of these deductions.

Withholding. A servicemember who quali-

es for the deduction on line 26 or a civil-

ian spouse who qualies for the deduction

on line 27 can complete form IT 4 to avoid

Ohio withholding on income not subject to

tax. Such taxpayers should check the ap-

propriate box in Section III of the IT 4 and

provide the form to their employers.

Filing. Certain military service members

may not have a ling requirement due to

the deductions available under Ohio law.

However, the Department recommends

that such taxpayers le an Ohio IT 1040

or IT 10 to avoid delinquency billings. For

more information on who must le an Ohio

income tax return, see page 11.

Extensions to File/Pay. Generally, Ohio

recognizes any extensions granted by the

IRS. Certain military servicemembers will

have the same extensions to le their Ohio

returns and pay any Ohio tax due. These

servicemembers do not owe interest, pen-

alties, or the interest penalty in connec-

tion with this extension period. See R.C.

5747.026 for more information.

Taxability. The charts below summarize

the taxability of income for military service-

members and their civilian spouses.

School District Income Tax. Military ser-

vicemembers and their civilian spouses

may be liable for school district income tax

if they are Ohio residents, even if they are

not present in Ohio due to military orders.

To determine if you are liable for school dis-

trict income tax, see page 46.

9

activities of the business during the taxable

year in which the sale occurs or during any

of the ve preceding taxable years.

Generally, income recognized by a sole

proprietorship or pass-through entity is

business income. However, determining

if income is business income is highly

dependent upon the specific facts and

circumstances.

What Are Some Examples of Business

Income vs. Nonbusiness Income?

Interest and Dividends: John reports

$1,500 of interest and dividend income on

federal Schedule B. $200 of his interest

income is from a pass-through entity that

primarily operates an investment business.

The remaining $1,300 is from personal,

nonbusiness sources. Thus, only $200 of

John’s interest is business income.

Capital Gains and Losses: Andrew rec-

ognizes a capital gain from the sale of a

tractor used to harvest wheat on his farm.

Since the tractor was integral to his farming

business, the capital gain is business

income.

Capital Gains and Losses: Paul reports

$8,000 of capital gain income on his

federal Schedule D. $2,000 of the capital

gains are from a pass-through entity that

primarily operates an investment business.

The remaining $6,000 is from personal,

nonbusiness sources. Thus, only $2,000 of

Paul’s capital gains are business income.

Rental Income and Losses: Debbie owns

a rental property. She actively advertises,

manages, and maintains the property.

Debbie is in the trade or business of property

rental. Therefore, her rental income is

business income.

Rental Income and Losses: Ryan

occupies a home on a golf course. The

golf course hosts a two-week tournament

every year. Ryan annually takes a vacation

to Florida and rents out his home during

the tournament. While the rental might be

considered regular, Ryan is not in the trade

or business of property rental. Therefore,

his rental income is not business income.

Royalty Income: Hannah works full-time

from her home writing children’s books.

Hannah has an agreement with a publisher

that pays her a royalty for each copy of her

book that is sold. Hannah is in the trade or

business of writing books. Therefore, her

royalty income is business income.

How Is Business Income Treated on My

Ohio Return?

Taxpayers can deduct the rst $250,000

($125,000 for married separate lers) of their

business income included in their federal

adjusted gross income. Also, any business

income not deducted is taxed at a at 3%.

See the instructions for the Ohio Schedule

IT BUS on page 19.

Additionally, Ohio-related business income

earned by nonresidents is taxable to Ohio.

See the instructions for the IT NRC on page 23.

How Does Ohio Law Dene Business

and Nonbusiness Income?

"Business income" is income, including gain/

loss, arising from any of the following:

● Transactions, activities, and sources in

the regular course of a trade or business

operation;

● Real, tangible, and intangible property

if the acquisition, rental, management,

and disposition of the property constitute

integral parts of the regular course of a

trade or business operation;

● A partial or complete liquidation of a busi-

ness, including gain or loss from the sale

or other disposition of goodwill;

● Income from certain sales of equity or

ownership interests in a business; OR

● Compensation and guaranteed pay-

ments paid by a pass-through entity, or

a professional employer organization on

its behalf, to an investor who directly or

indirectly owns 20% or more of the entity.

"Nonbusiness income" is any income other

than business income.

See R.C. 5747.01(B), 5747.01(C) and

5733.40(A)(7).

How Do I Determine What Income Is

Business Income?

Business income can be determined by

using either test:

Transactional Test: Looks to the nature,

frequency and regularity of the transaction.

Functional Test: Looks to if the property

was integral to the trade or business, or if

it generated business income in the past.

See Kemppel v. Zaino, 2001-Ohio-92.

Sale of an equity or ownership interest in a

business means the sale was treated as an

asset sale for federal income tax purposes

and/or the seller materially participated,

as described in 26 C.F.R. 1.469-5T, in the

Mineral Rights Income: Cynthia allows

a company to extract minerals from her

residential property. She receives income

based on the company's usage of her land.

Since Cynthia is not engaged in a trade or

business related to this income, it is not

business income.

Pass-Through Income: Ellen owns 15% of

a pass-through entity. She reports $50,000

of ordinary income, $10,000 of bonus

depreciation, and $60,000 of guaranteed

payments on federal Schedule E. Since

Ellen owns less than 20% of the entity, the

guaranteed payments are nonbusiness

income. Thus, her net business income from

federal Schedule E is $40,000 (her ordinary

income less bonus depreciation).

Guaranteed Payments: Stan owns 25% of

a pass-through entity. He reports a $60,000

guaranteed payment on federal Schedule

E. Because he owns at least 20% of the

entity, the guaranteed payment is business

income.

Wages/Compensation: Jim owns 80% of

an S corporation. Jim receives $200,000 of

wages from the S corporation, which are

reported on a W-2. Because he owns at

least 20% of the corporation, the wages are

reclassied as business income.

Trust Income: Brett sets up a trust, with

himself as the beneciary, that invests in

multiple pass-through entities. Operating

income from these entities is distributed

to the trust, which further distributes the

income to Brett. Since the income was

business income to the entities, it retains its

character as business income as it passes

through to the trust and to Brett.

Trust Income: David sets up a trust, with

himself as the beneficiary, to hold his

personal investments. Although David uses

a trust, the usage of a trust does not create a

trade or business. Therefore, the investment

income is nonbusiness income to both the

trust and to David.

For more information, see the "Income – Business Income and the Business Income Deduction" topic at tax.ohio.gov/FAQ.

.

2022 Ohio IT 1040 / SD 100

10

General Information for the Ohio IT 1040

How Do I Show I Am a Nonresident of

Ohio?

Any individual can challenge the pre-

sumption of Ohio residency by providing

documentation showing that they are a

nonresident. Ohio uses a contact period test

to determine the burden of proof needed to

show that an individual is a nonresident.

If you had fewer than 213 contact periods

in Ohio during the tax year, you must

provide enough documentation to show

that it is more likely than not that you were

a nonresident. If you had 213 or more

contact periods, you must provide clear and

convincing documentation that you were a

nonresident.

Alternatively, certain individuals can change

the presumption of Ohio residency to a

presumption of nonresidency by ling the

Ohio Nonresident Statement (form IT NRS).

For more information on this statement, see

pages 13 and 49.

See R.C. 5747.24(B), (C) and (D).

What Is a Contact Period?

You have a contact period in Ohio if all of

the following are true:

● You have an abode outside of Ohio;

● You are away overnight from your abode;

AND

● While away, you spend any portion of two

consecutive days in Ohio.

You do not have to spend the night in

Ohio. For example, if you spend portions of

Monday and Tuesday in Ohio, but stay in

a hotel in Kentucky on Monday night, you

would still have a contact period in Ohio.

You must spend consecutive days in Ohio to

have a contact period. For example, if you

spend portions of Monday and Wednesday

in Ohio, but not Tuesday, then you would not

have a contact period in Ohio.

See R.C. 5747.24(A).

Who Must File an Ohio Income Tax

Return?

Every Ohio resident and every part-year

resident is subject to the Ohio income tax.

Every nonresident having Ohio-sourced

income must also le. Examples of Ohio-

sourced income include the following:

● Wages or other compensation earned in

Ohio (see "Exception" below);

● Ohio lottery winnings;

● Ohio casino gaming winnings;

● Income or gain from Ohio property;

● Income or gain from a sole proprietorship

doing business in Ohio;

● Income or gain from a pass-through entity

doing business in Ohio.

Exception: A full-year nonresident living in

Indiana, Kentucky, Michigan, Pennsylvania,

or West Virginia does not have to le if the

nonresident's only Ohio-sourced income is

wages.

Example: Charley lives in Kentucky but

commutes to Cincinnati every day to her

job. Charley's wages are not taxable in Ohio

even though they are earned here.

tax return if:

● Your Ohio adjusted gross income (Ohio

IT 1040, line 3) is less than or equal to $0;

● The total of your senior citizen credit,

lump sum distribution credit, and joint l-

ing credit (Ohio Schedule of Credits, lines

4, 5 and 12) is equal to or exceeds your

income tax liability (Ohio IT 1040, line 8c)

and you are not liable for school district

income tax; OR

● Your exemption amount (Ohio IT 1040,

line 4) is the same as or more than your

Ohio adjusted gross income (Ohio IT

1040, line 3).

However, even if you meet one of these ex-

ceptions, if you have a school district income

tax liability (SD 100, line 2), you are required

to le the Ohio IT 1040.

Note: If your federal adjusted gross income

is greater than $28,450, the Department

recommends that you file an Ohio IT

1040 or IT 10, even if you do not owe

any tax, to avoid delinquency billings.

Ohio IT 10: Certain taxpayers can le Ohio

form IT 10 instead of the Ohio IT 1040. The

four types of taxpayers described on form IT

10 are eligible to le the form if they:

● Do not have an Ohio individual income

or school district income tax liability; AND

● Are not requesting a refund.

Do not le the IT 10 if you le the IT 1040.

See R.C. 5747.08.

Ohio Residency

What Is my Ohio Residency Status?

Resident: You are an Ohio resident for

income tax purposes if you are domiciled

in Ohio. Thus, under Ohio law, the terms

“domiciled” and “resident” mean the same

thing.

Generally, any individual with an abode

in Ohio is presumed to be a resident. The

abode can be either owned or rented.

Temporary absence from your Ohio abode,

no matter how long, does not change your

residency status. Thus, if you live in Ohio,

the presumption is that you are an Ohio

resident.

Example: Brent travels to Florida each

winter and returns to Ohio each spring.

However, he maintains his Ohio driver's

license, voter registration, etc. and has not

established permanent residence in Florida.

Therefore, he is a full-year resident of Ohio.

Part-year resident: You are a part-year

resident of Ohio if you were a resident of

Ohio for a portion of the tax year and a

nonresident for the rest of the tax year.

Thus, you are a part-year resident if you

permanently moved into or out of Ohio

during the tax year.

Part-year residents are entitled to the

nonresident credit for any income earned

while they were a resident of another state.

They are also eligible for the resident credit

on non-Ohio income earned while they were

an Ohio resident, if they were subject to, and

paid tax on, that income in another state.

Nonresident: You are a nonresident if you

were a resident of another state for the entire

tax year. Nonresidents who earn or receive

income within Ohio will be able to claim the

nonresident credit with respect to all items of

income not earned and not received in Ohio.

If you are currently a member of the

military and you have questions about your

residency status, see page 9.

For more information, see tax.ohio.gov/

residency, or Information Release IT

2018-01, "Residency Guidelines - Tax

Imposed on Resident and Nonresident

Individuals for Taxable Years 2018 and

Forward." See also R.C. 5747.01(I)(1) and

Cunningham v. Testa, 2015-Ohio-2744.

2022 Ohio IT 1040

11

Wildlife Species and

Endangered Wildlife

The Division of Wildlife uses these funds to

establish habitat and protect open spaces

for wildlife. Past donations have helped to

restore populations of endangered species.

Your generous donation will continue to help

support Ohio's native wildlife – a natural

treasure!

If you do not have an overpayment on your

Ohio IT 1040, but you want to donate to

provide grants to protect Ohio's natural

heritage, you may do so by writing a check

payable to the "Nongame and Endangered

Wildlife Special Account" and mailing it to:

Ohio Department of Natural Resources

Division of Wildlife

2045 Morse Road, Building G-1

Columbus, OH 43229-6693

To learn more, go to wildlife.ohiodnr.gov.

Wishes for Sick Children

Contributions are distributed by the Ohio

Department of Health to fund a program

administered by a nonprot corporation that

grants the wishes of individuals who are

under the age of 18, Ohio residents, and

have been diagnosed with a life-threatening

medical condition.

If you do not have an overpayment on your

Ohio IT 1040, but you want to donate to

provide funds for Wishes for Sick Children,

you may do so by writing a check payable to

"Ohio Treasurer of State" or "Ohio Depart-

ment of Health" and mailing it to:

Ohio Department of Health

Attn: Wishes for Sick Children

P.O. Box 15278

Columbus, OH 43215-0278

A donation will reduce the

amount of the refund that

you are due. If you decide to

You cannot change your

mind and later ask for your donations to

be refunded. If you do not want to donate,

do not enter an amount on Ohio IT 1040,

lines 26a-g.

Because your tax return is condential, the

Department cannot release your name to the

fund administrators, but the administrators

extend appreciation to those who donate.

Your donation may be tax-deductible on a

future federal income tax return.

See R.C. 5747.113.

Contributions made to the project are used

to provide free breast and cervical cancer

screening, diagnostic and outreach/case

management services to uninsured and

underinsured Ohio women. The project is

administered by the Ohio Department of

Health and is operated through 11 regional

agencies, which enroll women in the pro-

gram and schedule them for services with

clinical providers in the agency's service

area.

If you do not have an overpayment on your

Ohio IT 1040, but you want to donate to

provide grants for free breast and cervical

cancer screening, you may do so by writ-

ing a check payable to "Ohio Treasurer of

State" or "Ohio Department of Health" and

mailing it to:

Ohio Department of Health

Attn: Breast & Cervical Cancer

P.O. Box 15278

Columbus, Ohio 43215-0278

In the description on the check, please write

"Breast and Cervical Cancer Donation."

The Military Injury Relief Fund provides

grants to individuals injured while in active

service as a member of the U.S. armed

forces and to individuals diagnosed with

post-traumatic stress disorder while serving,

or after having served, in Operation Iraqi

Freedom, Operation New Dawn or Opera-

tion Enduring Freedom.

Donations that Apply to Ohio IT 1040

If you do not have an overpayment on your

Ohio IT 1040, but you want to donate to

provide grants to such individuals, you may

do so by writing a check payable to "Ohio

Treasurer of State (ODVS)" and mailing it to:

Ohio Department of Veterans Services

Military Injury Relief Fund

P.O. Box 373

Sandusky, OH 44871

Ohio History Fund

The Ohio History Fund is a 501(c)(3) non-

prot organization that allocates these funds

toward a matching grants program to sup-

port state and local history-related projects

throughout Ohio.

If you do not have an overpayment on

your Ohio IT 1040, but you want to donate

to provide grants to promote and protect

Ohio's rich history, you may do so by writ-

ing a check payable to "The Ohio History

Connection Income Tax Contribution Fund"

and mailing it to:

The Ohio History Connection

Attn: Business Oce

800 E. 17th Avenue

Columbus, OH 43211-2474

Donations may also be made online at

www.ohiohistory.org.

State Nature Preserves and

Scenic Rivers

Contributions are used to protect Ohio's

state nature preserves, scenic rivers, rare

species and unique habitats. Your donations

play a critical role in caring for Ohio's most

exceptional forests, wetlands, prairies, rivers

and streams. Donations fund educational

outreach programs, research and monitoring

for rare species and construction of facilities

that improve public access.

If you do not have an overpayment on

your Ohio IT 1040, direct donations may

also be made by check or online. Please

visit the "Support Natural Areas" section

at naturepreserves.ohiodnr.gov for

information.

2022 Ohio IT 1040

!

CAUTION

12

School District Number

If you were an Ohio resident for any part of

the tax year, enter the number of the school

district in which you lived during the majority

of the year. Full-year nonresidents should

enter 9999.

See pages 40-45 for a full list of Ohio’s

school districts or use The Finder at tax.

ohio.gov/Finder.

Note: Some school districts levy an income

tax on their residents. See page 46 for more

information.

Residency Status

Check the box corresponding to your resi-

dency status. If your ling status is married

ling jointly, each spouse must indicate his/

her residency status.

If you checked the box for "part-year resi-

dent" or “nonresident,” write, in the space

provided, the two-letter abbreviation of the

state where you resided for the majority of

the tax year.

For more information on Ohio residency,

see page 11.

Ohio Nonresident Statement

Nonresidents who meet certain required

criteria and wish to establish an irrebuttable

presumption of non-Ohio residency for the

tax year may check these boxes instead

of ling form IT NRS. The

criteria are listed on page 49 under the

heading, “What Criteria are Required to File

the Ohio Nonresident Statement?”

Nonresidents who le jointly and both meet

the required criteria can each check the

appropriate box to establish an irrebuttable

presumption of non-Ohio residency.

Note: Individuals who do not meet the

required criteria are still able to le as non-

residents. Residents and part-year residents

cannot check these boxes to establish

an irrebuttable presumption of non-Ohio

residency.

Extension Filer

Any taxpayer with a valid federal extension

is allowed an extension of time to le their

Ohio returns. Such taxpayers should check

the box indicating they are a federal exten-

sion ler for this tax year to qualify for the

Ohio extension. For more information on

ling extensions, see page 7.

School District Number

Enter the school district number for which

you are ling this return on pages 1 and

2. See pages 40-45 for a full list of Ohio’s

school districts or use The Finder at tax.

ohio.gov/Finder.

School District Residency Status

Check the box corresponding to your resi-

dency status for the school district number

you entered on the return. If you are a part-

year resident, enter the dates of residency.

Tax Type

Check the box indicating the tax type of the

school district for which you are ling this

return. The list of school districts on pages

40-45 indicates the tax type of each taxing

school district.

For more information on the two tax types,

see page 46.

Amended Return Check Box

Check this box if you are amending your

previously led return. You must include

the Ohio IT RE and/or SD RE with your

amended return. See page 8 for amended

return instructions. This box is not available

on form IT 10.

Net Operating Loss (NOL) Check Box

Check this box if you are amending due to

a net operating loss carryback. You must

include the Ohio Schedule IT NOL with your

amended return. This box is not available

on form IT 10.

Name(s), Address and SSN(s)

Enter your name and current address on

page 1 and your SSN on pages 1 and 2 of

your return (if ling jointly, also enter your

spouse’s name and SSN on page 1). Do not

include your spouse’s name and SSN if

Note: If you and/or your spouse have an

Individual Taxpayer Identication Number

(ITIN), you should enter the ITIN in the

spaces provided on the return for the SSN.

County

If you were an Ohio resident for any part of

the tax year, enter the rst four letters of the

county in which you lived during the major-

ity of the tax year. Full-year nonresidents

should leave these boxes blank.

Filing Status

Your ling status must be the same as your

federal income tax ling status for the tax

year. See R.C. 5747.08(E).

If you check “married ling separately,” enter

your spouse’s SSN in the spaces provided.

must

return even if one or both of

you are nonresidents of Ohio.

You may claim the nonresident credit

(see the Ohio Schedule of Credits) for

income not earned or received in Ohio.

federal returns, you must

Ohio returns.

!

CAUTION

Completing the Top Portion of Your Ohio Returns

These instructions are used to complete the top portions of the Ohio IT 1040, SD 100, and IT 10.

2022 Ohio IT 1040 / SD 100 / IT 10

IT 1040, SD 100 and IT 10 IT 1040 and IT 10 SD 100 Only

13

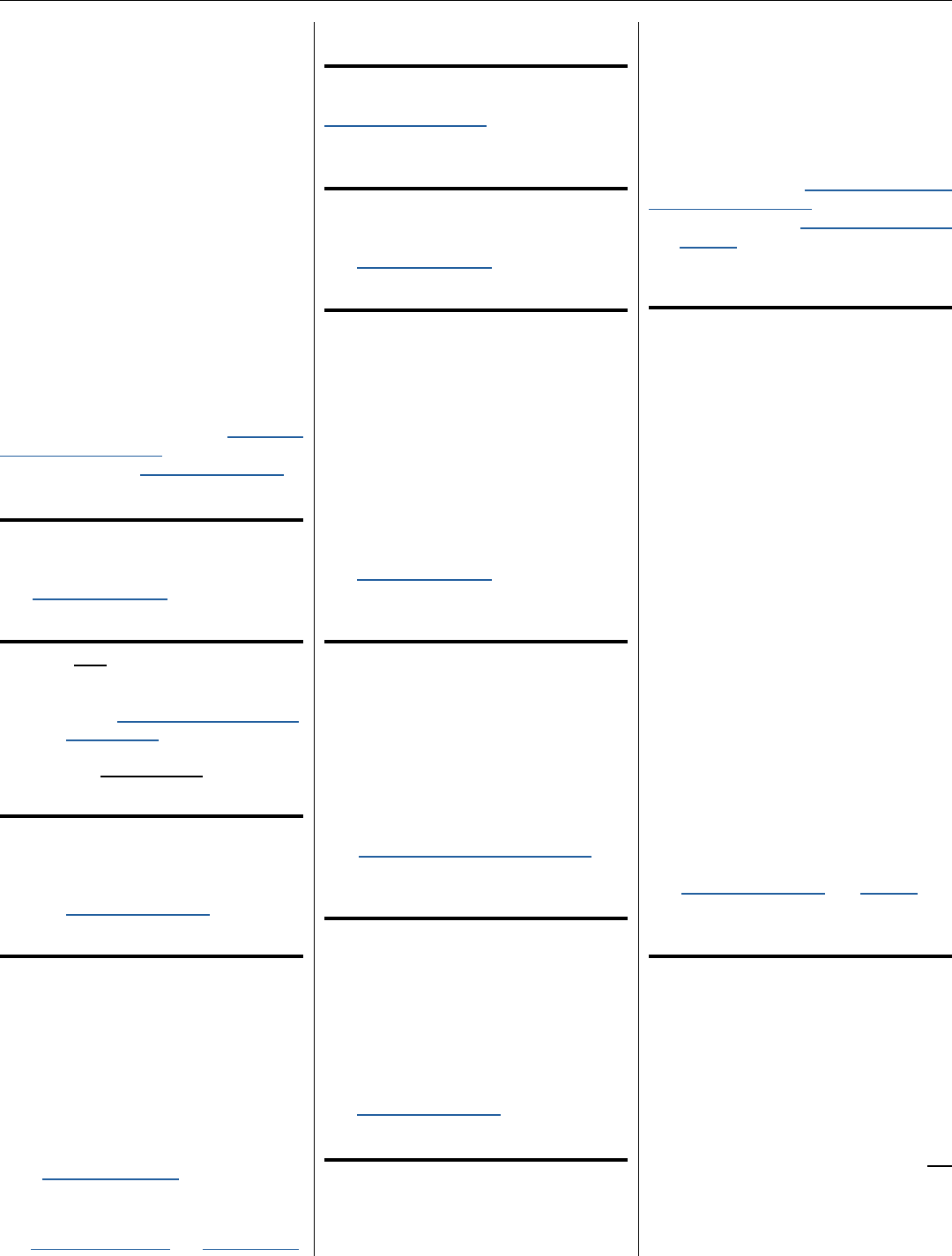

Line 4 – Personal and Dependent

Exemptions

Ohio allows an exemption for the following:

● You, if not claimed as a dependent on

another person’s return;

● Your spouse, if filing jointly and not

claimed as a dependent on another per-

son’s return; AND

● Your dependents claimed on your federal

tax return.

The personal and dependent exemption is

based on your modied adjusted gross in-

come (see page 7):

Enter your number of exemptions in the

spaces provided. Multiply your exemptions

by the appropriate amount from above and

enter the result on line 4.

Example: John and Mary claim their son

Patrick as an exemption on their jointly led

federal income tax return. Their modied

adjusted gross income is $75,000. Thus,

they claim three exemptions totaling $6,450

on their Ohio return. Patrick les his own

tax return. Since Patrick is a dependent

and his parents claim an exemption for him,

he is not eligible for an exemption on his

return. He should check the box indicating

he can be claimed by someone else and

enter $0 on line 4.

Ohio Schedule of Dependents. If you

included dependents on your Ohio re-

turn, complete the Ohio Schedule of De-

pendents. If your dependent has an indi-

vidual tax identication number (ITIN) or

adoption taxpayer identication number

(ATIN), enter that number in the boxes for

the dependent's SSN. If the dependent

information is not provided, incomplete,

or contains errors, you may be asked for

supporting documentation.

See R.C. 5747.025 and 5747.01(O).

Line 8a – Tax on Line 7a

Calculate your tax on your Ohio income tax

base less business income.

● All taxpayers can utilize the Income Tax

Brackets found on page 31.

● If your nonbusiness taxable income is

less than $115,300, your tax has been

calculated for you in the Income Tax Table

found on pages 32-37.

Line 1 – Federal Adjusted Gross

Income

Enter the amount from your 2022 federal

income tax return:

● Federal 1040, line 11;

● Federal 1040-SR, line 11; OR

● Federal 1040-NR, line 11.

Generally, line 1 of your Ohio

income tax return must match

-

Revenue Code.

Income. If you have a zero or negative

federal adjusted gross income, you must

include a copy of page 1 of your federal

return.

A foreign trust that les federal form 1040-

NR should not use the IT 1040 to le with

Ohio. Such trusts must le form IT 1041.

See R.C. 5747.01(A).

Line 2a – Ohio Schedule of Adjust-

ments (Additions)

The Ohio Schedule of Adjustments lists

the additions to your federal adjusted

gross income. For more information

about the additions you must make, see

pages 15-16.

● If you have no additions to your Ohio

income, leave line 2a blank.

● Any additions listed on this line must be

supported by the applicable Schedule

of Adjustments line item(s). Enter the

amount from Schedule of Adjustments,

line 10 on this line.

You must include a copy of the Ohio

Schedule of Adjustments with your return.

Line 2b – Ohio Schedule of

Adjustments (Deductions)

The Ohio Schedule of Adjustments lists

the deductions from your federal adjusted

gross income. For more information about

the deductions you must make, see pages

16-19.

● If you have no deductions to your Ohio

income, leave line 2b blank.

● Any deductions listed on this line must

be supported by the applicable Schedule

of Adjustments line item(s). Enter the

amount from Schedule of Adjustments,

line 39 on this line.

You must include a copy of the Ohio

Schedule of Adjustments with your return.

Note: The tax amount listed in the Income

Tax Table may be slightly lower or higher

than the tax amount computed by using the

Income Tax Brackets.

See R.C. 5747.02(A)(3).

Line 11 – Interest Penalty

Generally, if you are a wage earner and have

Ohio withholding, you will not owe an interest

penalty. If you have non-wage income or

no Ohio withholding, use Ohio IT/SD 2210

to determine if an interest penalty is due.

For more information, see the "Income -

Estimated Income/School District Taxes

and the 2210 Interest Penalty" topic at tax.

ohio.gov/FAQ. See also R.C. 5747.09(D)

and (E).

Line 12 – Unpaid Use (Sales) Tax

Report the amount of unpaid use (sales)

tax due for the tax year. You owe Ohio use

tax if both of the following are true:

● You made purchases where sales tax

was not collected; AND

● The purchases were not qualifying

purchases made during Ohio's sales

tax holiday.

Use tax eliminates the disadvantage to

Ohio retailers when Ohio shoppers buy

from out-of-state sellers who do not col-

lect sales tax. Use tax is most commonly

due on out-of-state purchases such as

those made from the internet, television,

or catalogs.

Use the worksheet on page 31 to calculate

your use tax. For more information, see the

"Sales and Use Tax" topics at tax.ohio.

gov/FAQ. See also R.C. 5747.083.

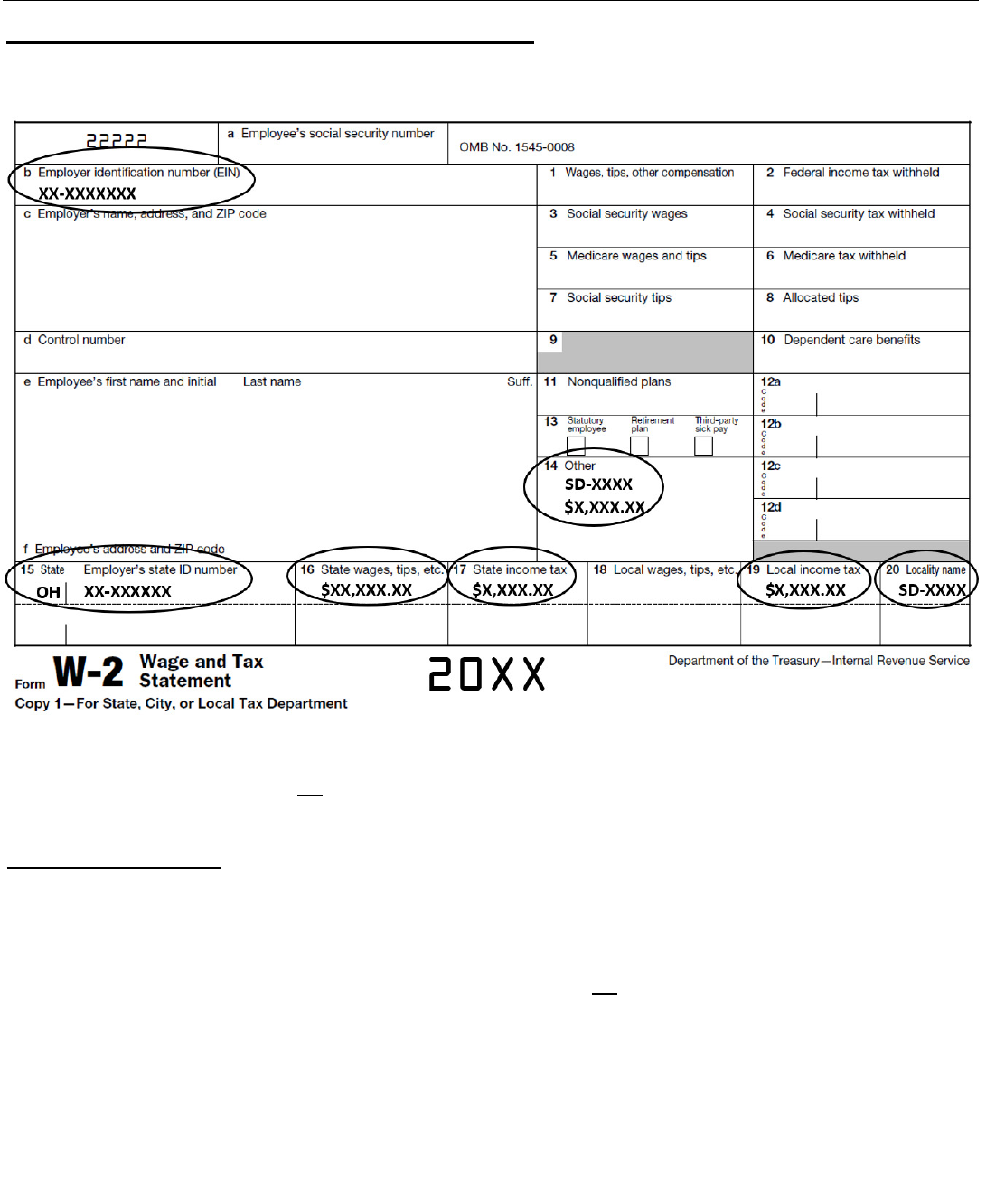

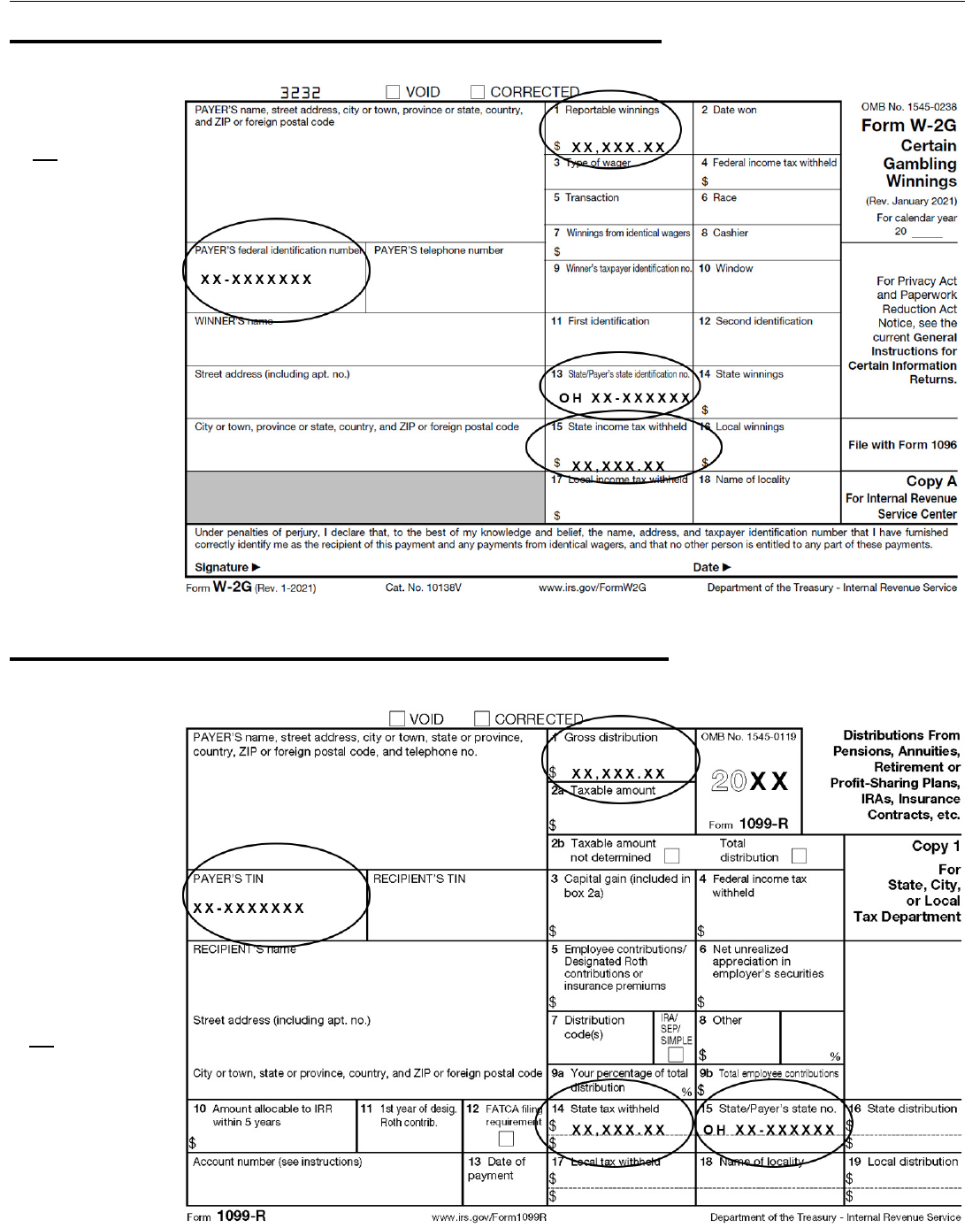

Line 14 – Ohio Income Tax Withheld

Enter your Ohio income tax withheld as

reported on Part A, line 1 of the Schedule

of Ohio Withholding.

Schedule of Ohio Withholding. Complete

this schedule if you are reporting an amount

on line 14 of the IT 1040. Enter only income

statements (W-2, W-2G, 1099) reporting

Ohio income tax withheld. Do not include:

● Taxes withheld for another state, a city, or

a school district; OR

● Taxes paid by a pass-through entity and

reported to you on an Ohio IT K-1 (report

these amounts on Ohio Schedule of

Credits, line 38).

See the sample statements on pages 38-39.

Do not list income statements that do not

report Ohio income tax withheld.

Place the state copies of your income

statements after the last page of your return.

Do not include income statements that are

handwritten, self-created, or generated by

your tax preparation software.

See R.C. 5747.08(H).

!

CAUTION

2022 Ohio IT 1040

Ohio IT 1040 - Individual Income Tax Return

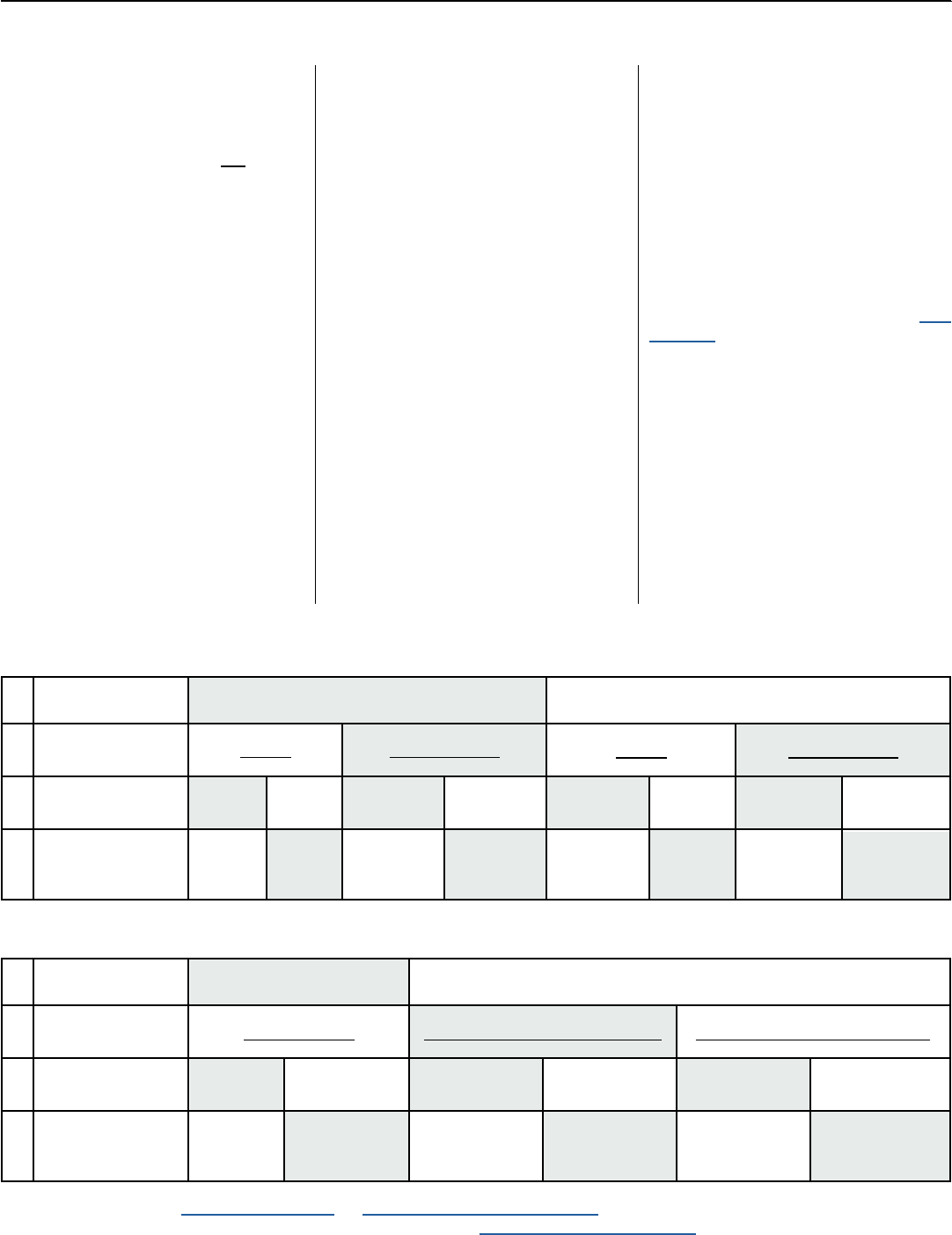

Gross Income

Personal/

Dependent

Exemption

$40,000 or less

$40,001 – $80,000

More than $80,000

$2,400

$2,150

$1,900

14

Line 26 – Donations

You may donate all or a portion of the

amount on line 24 to one or more of the

organizations listed. Such donations will

reduce your refund, and are only allowed

on timely led, original returns; they are not

allowed on amended returns.

If you decide to donate, this decision is

. For more information on the donation

options, see page 12.

See also R.C. 5747.113.

Line 27 – Your Refund

If you do not request direct deposit, or you

led by paper, your refund will be mailed to

the address on the tax return.

Note: Your refund may be oset pursuant

to R.C. 5747.12. You will be notied if your

refund is subject to oset.

your refund may be delayed. Notify the

Department of your address change as

soon as possible.

Line 22 – Interest Due

Interest is due from the unextended due date

until the date the tax is paid. Generally, you

do not owe interest if you are due a refund.

An extension of time to le does not extend

the payment due date. The interest rate for

calendar year 2023 is 5%.

Certain military servicemembers may not

be subject to interest. See page 9 for more

information.

See R.C. 5747.08(G).

Line 23 – Total Amount Due

This amount must be paid by April 18,

2023. Do not mail cash. Instead, make

payment by:

● Electronic check;

● Credit or debit card; OR

● Paper check or

money order.

Make your check or money order payable

to "Ohio Treasurer of State" and include an

Ohio IT 40P or IT 40XP payment voucher.

Include the tax year and the last four digits

of your SSN on the “Memo” line.

For more information regarding payment

options, see page 6.

Line 25 - Credit Carryforward

Enter the portion of your refund you want

applied to tax year 2023. This is only al-

lowed on timely led, original returns; it is

not allowed on amended returns.

Line 15 – Payments and Credit

Carryforward Amounts

Enter the following amounts:

● Estimated payments (Ohio IT 1040ES);

● Extension payments (Ohio IT 40P); AND

● Any credit carryforward amount from your

prior year Ohio IT 1040.

Do not include:

● A prior year's refund that you requested

but did not receive. Contact the Depart-

ment about the status of any such refund.

● Taxes paid by a pass-through entity and

reported to you on an Ohio IT K-1 (report

these amounts on Ohio Schedule of

Credits, line 38).

See R.C. 5747.09(B).

Line 17 – Amount Previously Paid

(Amended Returns Only)

When ling an amended return, enter the

amount previously paid with your previously

led return(s) excluding the amount reported

on line 15.

Line 19 – Overpayment Previously

Requested (Amended Returns Only)

When ling an amended return, enter the

amount you reported on line 24 on your

previously led return(s).

2022 Ohio IT 1040 / Schedule of Adjustments

Additions

Line 1 – Non-Ohio State or Local

Government Interest and Dividends

Enter interest and/or dividends paid on

obligations or securities from a non-Ohio

state, city, county, or other local government.

Do not include:

● Any amounts already included in federal

adjusted gross income;

● Amounts paid on obligations or securities

from Ohio, or an Ohio city, county, school

district, or other local government;

● Amounts paid on obligations or securi-

ties from a U.S. territory or the federal

government.

See R.C. 5747.01(A)(1).

Line 2 – Pass-Through Entity Add-Back

Enter Ohio pass-through entity tax (from the

IT 1140 and/or IT 4738) to the extent it was

deducted or excluded in arriving at your

federal adjusted gross income. The tax

may be reported to you on an Ohio IT K-1

or provided with the federal K-1. See R.C.

5747.01(A)(15) and (36).

Line 3 – College Tuition Expenses

Enter any amount reported to you on a

1099-Q representing distributions from the

Ohio CollegeAdvantage program that meet

all of the following:

● The amount is not otherwise included in

your federal adjusted gross income;

● The amount was not used to pay for quali-

ed higher-education expenses and was

not distributed due to the beneciary's

death, disability, or receipt of a scholar-

ship; AND

● The amount was deducted as an Ohio 529

plan contribution or tuition credit purchase

on the Ohio Schedule of Adjustments in

any tax year.

See R.C. 5747.01(A)(9) and 5747.70.

Line 4 – Ohio Public Obligations

Enter any loss resulting from the sale/dispo-

sition of Ohio public obligations to the extent

that such losses have been deducted in

determining federal adjusted gross income.

See R.C. 5747.01(A)(8).

Line 5 – Medical Savings Account

Enter amounts from a medical savings

account withdrawn for nonmedical pur-

poses only if the amount was deducted

on the Ohio Schedule of Adjustments in

any tax year. Use the worksheet on page

27 to calculate this adjustment. See R.C.

5747.01(A)(14).

Line 6 – Reimbursement of Expenses

Enter reimbursements received in 2022

for any expenses that you deducted on a

previously led Ohio income tax return if

the amount of the reimbursement was not

included in federal adjusted gross income for

2022. See R.C. 5747.01(A)(11)(b).

Line 7 – Accelerated Depreciation

Add 5/6 of your bonus depreciation allowed

under Internal Revenue Code section

168(k). Also add 5/6 of your depreciation

expense allowed under Internal Revenue

Code section 179 less the amount that

would have been allowed under section

179 as it existed on Dec. 31, 2002.

15

2022 Ohio Schedule of Adjustments

Replace “5/6” with “2/3” for employers who

increased their Ohio income taxes withheld

by an amount equal to or greater than 10%

over the previous year. Replace “5/6” with

“6/6” for taxpayers who incur a net operat-

ing loss for federal income tax purposes if

the loss was a result of the 168(k) and/or

179 depreciation expenses.

No add-back is required for:

● Employers who increased their Ohio

income taxes withheld over the previous

year by at least their total 168(k) and 179

depreciation expenses;

● 168(k) or 179 depreciation from a pass-

through entity in which the taxpayer owns

less than 5%.

This add-back is deductible on the Ohio

Schedule of Adjustments in future tax years.

Use the worksheet on page 28 to assist you

in calculating your future years' deductions.

For more information, see the "Income -

Bonus Depreciation" topic at tax.ohio.

gov/FAQ. See also R.C. 5747.01(A)(17).

Line 8 – Federal Interest and Dividends

Enter interest or dividends on obligations of

the U.S. government exempt from federal

taxation but not exempt from state taxation.

See R.C. 5747.01(A)(2).

Line 9 – Federal Conformity Additions

This line is only for federal conformity adjust-

ments. Do not enter any federal Schedule A

adjustments on this line. For updates on Ohio

conformity, see tax.ohio.gov/conformity.

See also R.C. 5701.11.

Deductions

Line 11 – Business Income Deduction

In order to take this deduction, you must

complete the Ohio Schedule IT BUS. See the

instructions on page 19. Enter the amount

from Ohio Schedule IT BUS, line 11, on this

line. See R.C. 5747.01(A)(28).

Line 12 – Reciprocity Wages

Enter compensation amounts earned in Ohio

during the portion of the year that you were

a resident of Indiana, Kentucky, Michigan,

Pennsylvania, and/or West Virginia. Do not

include any Ohio sourced business income,

lottery or casino winnings, rental or royalty in-

come, capital gains, or non-employee wages.

Exception: This deduction does not apply to

compensation from a pass-through entity in

which you directly or indirectly own at least

20%. R.C. 5733.40(A)(7) reclassies such

compensation as a distributive share of

income from the pass-through entity.

See R.C. 5747.01(A)(33) and 5747.05(A)(2).

Line 13 – State or Municipal Income Tax

Overpayments

Enter the amount from your 2022 federal

income tax return, Schedule 1, line 1. See

R.C. 5747.01(A)(11)(a).

Line 14 - Taxable Social Security

Benets

Deduct the amount on your federal 1040 or

1040-SR, line 6b. Do not enter any non-tax-

able portion of your Social Security benets.

See R.C. 5747.01(A)(5).