The Journal of Entrepreneurial Finance The Journal of Entrepreneurial Finance

Volume 12

Issue 2

Fall 2007

Article 5

December 2007

Tools to Apply to Financial Statements to Identify Errors, Tools to Apply to Financial Statements to Identify Errors,

Omissions and Fraud in Business Valuations Omissions and Fraud in Business Valuations

Tom Clevenger

Washburn University

Gary Baker

Washburn University

Follow this and additional works at: https://digitalcommons.pepperdine.edu/jef

Recommended Citation Recommended Citation

Clevenger, Tom and Baker, Gary (2007) "Tools to Apply to Financial Statements to Identify Errors,

Omissions and Fraud in Business Valuations,"

Journal of Entrepreneurial Finance and Business Ventures

:

Vol. 12: Iss. 2, pp. 75-86.

DOI: https://doi.org/10.57229/2373-1761.1028

Available at: https://digitalcommons.pepperdine.edu/jef/vol12/iss2/5

This Article is brought to you for free and open access by the Graziadio School of Business and Management at

Pepperdine Digital Commons. It has been accepted for inclusion in The Journal of Entrepreneurial Finance by an

authorized editor of Pepperdine Digital Commons. For more information, please contact

bailey[email protected].

Tools to Apply to Financial Statements

to Identify Errors, Omissions and Fraud

in Business Valuations

Tom Clevenger

*

Washburn University

and

Gary Baker

**

Washburn University

Often economists are asked to value businesses. Many times the information provided is

minimal and of questionable value. Data may be provided by parties wishing to bias the

valuation. The financial statements typically provided are balance sheets and income statements.

These sources can be fraught with errors, omissions and even fraud. The cash flow statements

derived from these statements can be misleading and any analysis from these spurious statements

is sure to be questioned.

A set of tools exist that can be used to establish the reliability of these financial

statements. Reliability is usually taken for granted in basic accounting and finance and reality is

often not as assumed. The tool kit uses basic accounting and mathematical logic. This logic,

teamed with basic accounting definitions and conventions, allows the economist some comfort

that the statements provided for use in the business valuation are free of obvious misinformation.

These tools can also help uncover some less detectable fraud.

*

Tom Clevenger is an Associate Professor of Accounting in the School of Business at Washburn University, in

Topeka, Kansas, USA. He holds a Doctorate of Business Administration from The University of Memphis. Dr.

Clevenger is also a Certified Public Accountant. In addition to his teaching Dr. Clevenger is a business advisor to

the Harrah’s Prairie Band Casino Gaming Commission.

**

Gary Baker is a Professor of Finance in the School of Business at Washburn University in Topeka, Kansas, USA.

He holds a Doctorate of Philosophy in Economics for the University of Nebraska. In addition to his teaching Dr.

Baker has a primary interest in the consulting firm Economic Research which specializes in computing economic

loss in injury and death cases. The firm also does some business valuations.

Tools to Apply to Financial Statements… (Clevenger& Baker)

76

For the analysis to proceed there must be two balance sheets and the intervening income

statement. By applying the accounting conventions and definitions, real, probable and possible

solutions are developed and explained. After examining the relationship between the financial

statements one is better able to value the business and be confident of the analysis.

Introduction

Most schemes used to hide business values are deceptively simple in origin and

operation. Being aware of the basic schemes makes the economist able to better judge a

businesses value. The existence of one or more of the schemes can lead the economist to seek

further information. The amounts of frauds sum to staggering amounts estimated at $660 billion

in annual losses in 2003.

1

Fraud exists. This is easily seen in the recent financial failures of large corporations such

as Enron to name one of many.

2

Regulatory reaction to these has been the Sarbanes-Oxley Act.

3

Regulatory action at such a level where professionals in accounting and auditing can be misled

indicate that caution is required at all levels of business valuation.

One can pick up any of the journals of the American Institute of Public Accountants’

“Journal of Accountancy”, the Institute of Internal Auditor’s “Internal Auditor”, the Institute of

Management Accountant’s “Strategic Finance”, and the American Association of Certified Fraud

Examiner’s “The White Paper” and “Fraud Magazine” and find reviews of the accounting basics

for these professionals related to fraud. Timely information is also found online through these

organizations. (www.aicpa.org, www.theiia.org, www.imanet.org, www.acfe.com) The Wall

Street Journal is another continuous source of financial misrepresentations. Frauds, large and

small, usually are not complex. Even the methods of manipulations are simple once exposed.

4

Having some tools to assist in the early detection can be of great usefulness in business

valuations for an economist.

Basic accounting and finance usually make the assumption that the information presented

is reliable. There exists the potential that bias exists in financial information provided by those

seeking to over value their assets or under value their business as the situation merits.

5

One can

use very basic assumptions to glean a comfort level about information the economist is given to

use in a business valuation.

6

Assumptions

This paper makes several assumptions: The business being valued will continue in

business for the foreseeable future; the financial information initially provided is minimal; the

material received may be of questionable character; and the information provided by the business

may be designed to bias the valuation.

The economist valuing the business must understand the financial statements may be less

than straightforward. Records and documents may be altered or created for purposes other than

1

“The Fight Against Fraud”, Internal Auditor, Salierno, D., (February 2005), pp. 62-66.

2

“SEC List of Accounting-Fraud Probe Grows”, The Wall Street Journal,(December 10, 2001), p. C1.

3

“A Price Worth Paying”, from The Economist print edition, May 19, 2005

http://www.economist.com/business/displayStory.cfm?story_id=3984019

4

“Confused About Earnings?”, Business Week, Byrnes, N. and Henry, D., (November 26, 2001), pp. 77 – 84.

5

“Many Companies Fail to Heed the SEC on Its Revenue-Recognition Guidelines”, The Wall Street Journal,

(December 14, 2000), pp. C1 and C4..

6

“The Stolen Guitar and Other Assets”, Fraud Magazine, A Publication of The Association of Certified Fraud

Examiners, Wells, Joseph, (May/June 2005) Vol. 1, No. 3, pp. 45–47 and 62.

The Journal of Entrepreneurial Finance & Business Ventures, Vol. 12, Iss. 2

77

valuing the business. Accounting principles are subject to interpretation and the application of

the principles may be aggressive or conservative depending on the person creating the

statements. The omission or addition of transactions may also alter the statements.

The income statement goal is to match the expenses incurred to the revenue generated.

This is the accrual method of accounting and to do this method four adjustments to timing of

revenues and expenses are needed whereby items are deferred or accrued. The adjustments when

misused are in revenue timing manipulation, asset value manipulation, expense concealment or

deferment and liability concealment.

The evaluator need only recognize that the accountant is accelerating or slowing revenues

or expenses appearance in financial records. These four accruals and deferrals are then offset to,

or from, the balance sheet. Such adjustments to the accounting records are reflected in the

ensuing financial statements. The preparer, by timing these adjustments near year-end, can

change completely the final reported results in the short run. WorldCom accomplished by

putting expenses on the balance sheet but even in doing so the revenues and earnings or net

income and cash flow were moving at different rates and directions indicating something was

amiss.

7

Income Statements and Balance Sheets

The income statement and balance sheets can be viewed as parts of a video game. The

income statement can be viewed as series of frames of a game. Each frame represents an event

or transaction. Revenues are points for the company and expenses are points for the opponent. If

the revenue for the period exceeds the expenses for the period the company wins. The excess of

the period is profits. Unlike sports, the excess or deficiency carries over to new periods as

retained earnings.

The balance sheet records the standing of the team before and after the game. Once the

standing of the player is determined the game restarts. The outcome of the game is subject to

manipulation by altering when the video stops and records the standings. The results of the

accrual method and the cash method of accounting produce the same results in the long run from

open to close of a business.

If the economist is concerned that the value of the business has been misrepresented then

one should look to the income statement of see if revenues are overstated, expenses are

understated, or both. The balance sheet needs to be examined to see if the value of the assets is

inflated or the value of liabilities minimized. Normally the assets are undervalued on the balance

sheet since the values are book values and not market values.

Example of Income Statement and Balance Sheet Manipulation.

The value of a company may be determined for several different reasons: adding a new

partner, a partner exits the business, a divorce, the sale of the business, bankruptcy, application

for a loan, or loss of earnings. In this example, the GT Company sells and services products in a

high tech field. The historical income statements and balance sheets are presented in tables I and

II respectively.

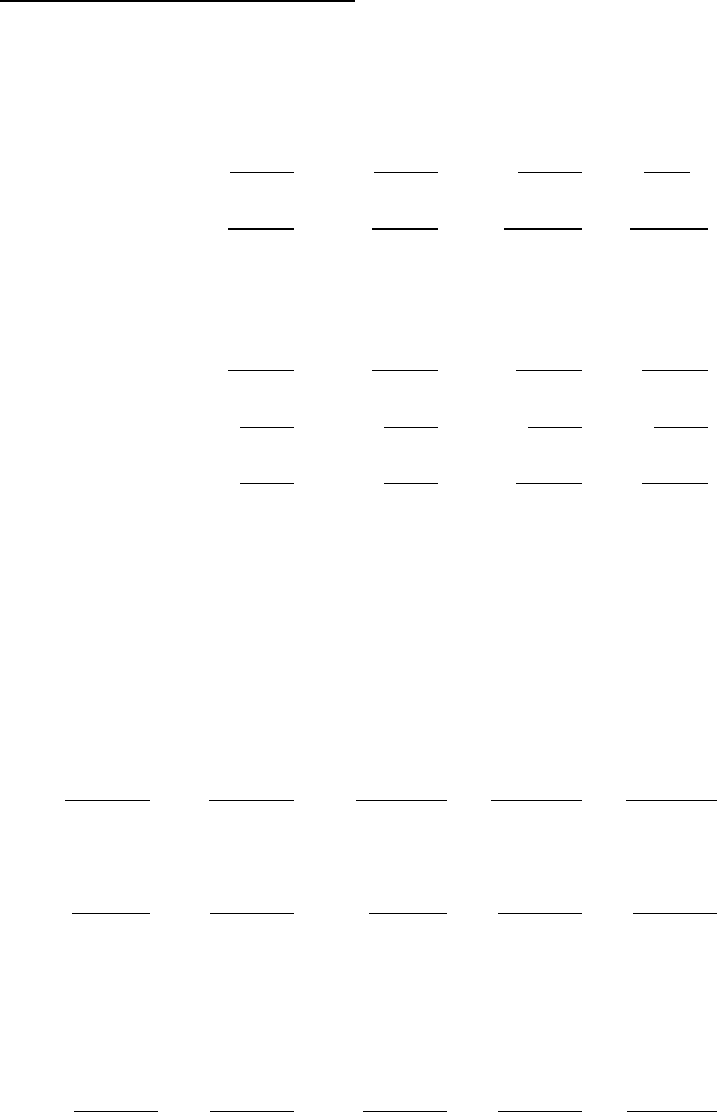

Table III presents selected ratios that suggest the firm is doing well. Assuming the value

of the firm is estimated by capitalizing the firm’s cash flow, the value of the firm has increased

7

2001 Annual Report for WorldCom, Inc., Consolidated Statement of Operations and Consolidated Statement of

Cash Flows.

Tools to Apply to Financial Statements… (Clevenger& Baker)

78

each year. If the capitalization rate is 20%, the value of the firm has increased from $67,000 in

2001 to $727,000 in 2004. Regardless of the capitalization rate, the value of the firm has

increased more than ten times from 2000 to 2004.

There should be some concern with the ratios for 2004. The gross profit margin in 2004

indicates a significant decrease in the cost of goods sold. While this might be possible through

technological advances, the change suggests further analysis is necessary.

Five additional ratios should also serve as red flags. The ratios are credit card expense as

a percent of sales, accounts receivable turnover, day’s accounts receivable outstanding, inventory

turnover and number of days to turn inventory. These ratios are presented in Table IV.

Credit card expense is the discount GT must pay the credit card company. Assume GT

pays 10% for each dollar of credit sales. During the years 2001, 2002 and 2003 credit card

expense was 5% of sales.

In 2001 the credit card expense of $5,000 means that credit sales were $50,000 for the

year. Credit sales for 2002 and 2003 were $75,000 and $105,000 respectively. In each year the

credit sales were about half of total sales.

In 2004 credit card expense was $13,000. If the same 5% applied then the credit sales

would be $130,000. If credit sales were one-half of total sales then total sales should be about

$260,000. However, sales are reported at $450,000. This means, a. errors exist, b. the firm had

an enormous increase in cash sales, or c. someone is falsifying sales documents. (Check cashing

company guarantee fees may also be used for such an indicator.)

The accounts receivable turnover has decreased from 6.67 times a year, or every 54.75

days to 1.48 times per year or every 247 days. This mean that credit has been extended to a

group of very poor paying customers or, perhaps the sales records are in error or are being

falsified.

Inventory turnover also indicates unusual activity. In 2001 the turnover was twice a year

or every 183 days. But in 2004 inventory turned over 25 time or every 14.6 days.

All of these ratios suggest that maybe games are being played in the sales area that is

fraudulent.

8

Industry ratios will also be helpful in this area for added analysis.

Related Income Statement and Balance Sheet Accounts

Understanding the relationship of income statement accounts and balance sheet related

accounts lends understanding to a business valuation. Two separate groups of accounts exist

with one group on the revenue and asset side and the other an expense and liability group.

The asset group consists of Sales Revenue, Trade Accounts Receivable, Other

Receivables and Cash Receipts. Cash Disbursements arise through Trade Purchases and Other

Expenditures passing through Trade Accounts Payable and Other Payables is the liability group.

These groups should always be considered using all interrelated accounts in its group and not just

one account in isolation.

Trade items make up the bulk of typical current transactions in these groups. Adding the

day’s sales in receivables to the day’s inventory purchases in payables gives an estimate of the

cash trade operating cycle. Comparing previous balance sheet estimates of this cycle with

current information gives the economist a position of insight. Significant deviations in cycle

times, actual cash flows and timing of cash flows may indicate manipulation in the financial

information provided in an income statement and balance sheet. The days of sales in receivables

8

“Irrational Ratios”, Wells, J., The Journal of Accountancy, (August 2001), pp. 80-83.

The Journal of Entrepreneurial Finance & Business Ventures, Vol. 12, Iss. 2

79

increasing might also exist. The significant increase in revenue should also be reflected in a

large increase in cash receipts.

Revenue and Gross Profit Manipulation

Revenue recognition is an area tools are needed for establishing the value of the business.

Over valuation can occur if sales revenues are recorded before sales are made, or an account

receivable is recorded that does not exist.

There are several examples that misrepresent revenues. A customer is permitted to take

an item from the store for a trial period, but is recorded as a sale. When goods shipped to a

customer are recorded as a sale and the goods were not ordered, makes a return likely. Goods are

sent to a retailer on consignment but the consignor recorded as sales the transaction as if the

goods were already sold by the consignee.

Another example of overvaluing a business is when sales revenues are recorded but did

not occur and the accompanying account receivable does not exist. This is out and out fraud

designed to improve the appearance of the company. Underlying accounting records reflect

timing of the recorded fictitious sales and receivables. Large additions to these accounts near

year-end need verification before continuing with the analysis. To under value a business the

sales may not be recorded. The most common occurrence is to not record cash sales and the cash

is skimmed before entering the business records. (Income tax consequences should be considered

in this instance.)

Large accounts receivables from a few customers also need review. If the following

accounting period shows the accounts were paid, then value probably exists. However, if there

are book adjustments, eliminating the receivables in the next period, the sales should be removed

from the proceeding period.

Cost of inventory is another tool to use when looking for manipulated revenues.

Significant increases in sales revenues should include significant changes in inventories.

Inventory changes can also be seen in differences from year to year in the current ratio and acid

test. Related to inventory cost is the cost of goods sold expense. A change in gross profit margin

is another red flag whether from increased sales or decreased cost of goods sold. One must find

out why a significant change in gross profit margin occurred.

Trade accounts payable, shown on the balance sheet, can be examined to see when the

inventory was purchased. One final method to increase gross profit is to purchase large amounts

of inventory for delivery before year-end. Ending inventory on hand is a reduction to cost of

goods sold in calculation and lowering this expense increases gross profit. Not recording the

corresponding accounts payable for the inventory is delayed until the next accounting period.

Gross profit increases net income and the added inventory increases total assets and

equity. Inventory could be returned the next period and the liability removed. However, the

overstatement from the last period now must be continued assuming business conditions remain

stable.

All methods mentioned do increase revenues and net income. Both balance sheet

accounts in asset and equity categories increase. Analysis made by the economist is affected in

an estimated over-valuation of the business. Key accounts the economist needs to put in the

toolkit are relating receivables and inventories to understand manipulated revenues.

Tools to Apply to Financial Statements… (Clevenger& Baker)

80

Expense Manipulation

Previously, manipulation examples of receivable and inventory accounts in revenue

schemes were presented. Writing off accounts receivable as not collectable is a way to remove

receivables created in a manipulation scheme. Using inactive accounts to charge goods as sold

and later remove it from these same inactive accounts through adjustment as bad debt expense is

one method. This method removes tangible goods and allows the expense to flow to income

statements as one intangible in nature. Inventory accounts are reasonable with sales and

purchases allowing goods removed to be converted to value outside of the normal business

channels. Actual business valuation will understate true worth in terms of cash flows.

True value of inventory can increase by not removing obsolete or unsalable items as

expense from the records and counting as in usable possession. Not recording sales returns (this

revenue account acts as an expense to reduce revenues) also maintains inventory at a level above

actual levels. Another inventory method is not recognizing warranty claims expenses for low

quality goods.

Ownership of inventory becomes important in some business agreements. Consigned

goods and special order goods have their own possible schemes for manipulation. Consigned

goods belong to the consignor and should not get included into inventory of consignee. Special

orders can be isolated by as little as a surrounding white line on the floor and counted as revenue

under certain circumstances. This same special order item could then be added back into ending

inventory to inflate the value of the inventory account by erasing the white line.

Add to these items the use of adjustment memos to create purchases, purchase returns,

and purchase allowances. Inventory itself can be kept as a long-term asset by adjusting the

current asset amount to a permanent account. Inventory turnover is a tool for use in examining

inventory. This ratio provides day’s inventory on hand for asset and expense comparison

purposes. It might also lead to seeking information on remaining assets.

Goodwill is a wonderful thing to increase the value of a business. It should not be

considered to exist unless there has been a purchase of an existing organization. Goodwill could

be a reflection of increasing certain assets to market value or simply the accounting records

increased based on perceived or desired amounts. Assigning values to existing tangible assets

should happen first and leftovers in a purchase price are considered goodwill. Goodwill created

in the first instance probably has little current value in the business valuation without substantive

verification. Proof of creation at onset is a wise course of action.

Goodwill created and kept on the records without amortization to the income statement

reduces the expenses and creates added income. Asset values remain constant and keep the

current ratio artificially level. Use of ratios excluding intangible items can be a tool to provide

confidence in this area. Other intangibles besides amortization needing substantiation include

royalties, patents, copyrights, and depletion. Research and development costs in certain instances

are immediate expenses and delayed in others. Careful consideration of circumstances is needed

in analyzing expensing or capitalizing such costs.

Putting expense items on the balance sheet can be accomplished with asset purchases and

leases. Asset values do not include interest on financing of the asset. Leasing an asset without

separating the inherent interest expense in the lease payment and putting the gross lease

payments amount, as asset value is a second method used to manipulate financial statements.

Another manipulation is recording a rental contract as if it were a purchase contract. Note that

the rental lease is an immediate expense and reduces the perceived value of profit and assets. The

tangible asset is touchable and could appear to be owned. Capitalizing expense items can occur

The Journal of Entrepreneurial Finance & Business Ventures, Vol. 12, Iss. 2

81

in very large dollar amounts. Sales of assets themselves might be recorded as sales revenue with

asset write-off unrecorded in a reverse scenario of putting income statement enhancements while

leaving assets unreduced.

Depreciation expense is a non-cash accounting estimate for allocating asset costs from

balance sheet to income statement. Merely recording depreciation expense and writing a check

for that amount has occurred. Economist can look at the year to year change of depreciation

expense. Changes in this expense and the balance sheet item “Accumulated Depreciation” will

indicate if asset changes occurred. Assets reported simply at some net amount without

depreciation explanation leaves much information out of an analysis. This intangible expense

should be separated from other non-cash expenses like depletion and amortization. All non-cash

expenses and intangible assets should be looked at in the records for activities rather than just

balances.

A reverse once again is the case of accretion as revenue in agriculture. Growth estimates

for a tree farm adjust for the value increase each period rather than expenses when planted and

revenues when harvested. However, this intangible revenue source and asset worth as true values

will not be known until the harvest does occur.

Expense and Liability Concealments

A transaction missing from the records is difficult to trace. Usually no trail is left to

follow. Missing liabilities are the hardest items to find in a business analysis. Something simple

as throwing away invoices from vendors before entering into the records does happen. It takes

time to discover such actions or for re-billings to show up or the debt may be written off by the

vendor if old enough. Bank records may be useful in looking for receipts and disbursements not

matching other accounting transactions.

Accounts Payable turnover is a tool to look at reasonableness of trade and other liabilities.

Existence of long-term liabilities might be discovered simply looking at interest expense. Size of

interest expense itself could indicate size of debt load unless interest payments are made outside

the business. Legal judgments for product liability or business negligence through the court

system are usually hard to detect. The information age allows much more timely investigations of

such potentials today.

Tax returns are a tool used to add support for the analysis. Tax return liabilities that are

constantly amended, audited or filed late should suggest internal problems. Why is this

occurring? Certainly, a tax return showing substantial tax losses while generating net incomes

and increasing retained earnings make financial statements suspect.

Foundation Tool

One basic tool is common through all previous income statement and balance sheet

manipulations. Two groups of related accounts included Cash Receipts and Cash Disbursements.

Accrual accounting adjusts business transactions from the cash method to the recognition of

revenues and matching of expenses based upon accounting rules. Using this very basic business

element of cash in and cash out leaves a balance that allows the economist to check outcome of

their analysis.

Net income and retained earnings cannot always be used to buy lunch or counted as cash.

These items capture truth or manipulation of other accounts and transactions in the current period

and summation of all periods. Cash flows attendant to these transactions is the final defense

against improper valuation. Cash flows constantly negative from normal operations or cash

flows not being generated from operations do not coexist with reality when earnings are reported.

Tools to Apply to Financial Statements… (Clevenger& Baker)

82

Periods of growth in earnings should also have some relation to cash flows from the underlying

transactions.

Summary

The economist has access or already knows the tools discussed in this analysis. Using

those tools in a different focus is what makes a new toolkit. Two balance sheets and one income

statement are minimums to use the tools. Tax returns and other business documents assist

making business valuations objective and defensible. Economists know many of the tools

presented here. What the economist can now do is apply these tools with added understanding of

the accounting conventions with which exist in financial statements.

The Journal of Entrepreneurial Finance & Business Ventures, Vol. 12, Iss. 2

83

REFERENCES

Aalberts, Robert J., Clauretie, Terrence. and Matoney, Joseph. “Small Business Valuation:

Goodwill and Covenants-Not-to-Compete in Community Property Divorce Claims.”

Journal of Forensic Economics, Fall 2000 Volume XIII, No. 3, Page 217 213

Accountancy, Journal of; American Institute of Certified Public Accounts, Harborside Financial

Center, Jersey City, NJ 07311-3881. (www.aicpa.org)

Arnold, Tom and James, Jerry: “Finding Firm Value “Quickly” with An Analysis of Debt,”

Journal of Financial Education, Vol. 29 Pages 65 –82. The Financial Education

Association, Nillanova, PA.

Byrnes, N. and Henry, D., “Confused About Earnings?”, Business Week, (November 26, 2001),

pp. 77 – 84.

Economist, The, “A Price Worth Paying”, from The Economist print edition, May 19, 2005

http://www.economist.com/business/displayStory.cfm?story_id=3984019

Internal Auditor, Institute of Internal Auditors, Danvers, MA 01923. (www.theiia.org)

Salierno, D., “The Fight Against Fraud”, Internal Auditor, (February 2005), pp. 62-66.

Strategic Finance, Institute of Management Accountants, Montvale, NJ 07645.

(www.imanet.org)

White Paper, The, and Fraud Magazine, Association of Certified Fraud Examiners, Austin, TX

78701 (www.acfe.com)

Wall Street Journal, The, “Many Companies Fail to Heed the SEC on Its Revenue-Recognition

Guidelines”, (December 14, 2000), pp. C1 and C4.

Wall Street Journal, “SEC List of Accounting-Fraud Probe Grows”,(December 10, 2001), p. C1.

Wall Street Journal, “SEC List of Accounting-Fraud Probe Grows” (December 10, 2001), p. C1.

Wells, Joseph, “Irrational Ratios”, The Journal of Accountancy, (August 2001), pp. 80-83.

Wells, Joseph, “The Stolen Guitar and Other Assets”, Fraud Magazine, A Publication of The

Association of Certified Fraud Examiners, (May/June 2005) Vol. 1, No. 3, pp. 45–47 and

62.

2001 Annual Report for WorldCom, Inc., Consolidated Statement of Operations and

Consolidated Statement of Cash Flows.

Tools to Apply to Financial Statements… (Clevenger& Baker)

84

Table I

Income Statements

Year 1 Year 2 Year 3 Year 4

Sales $100,000 $150,000 $210,000 $450,000

Cost of Good Sold 50,000 77,000 110,000 125,000

Gross Profit 50,000 73,000 100,000 325,000

Operating Expenses

Credit Card Expense 5,000 7,500 10,500 13,000

Depreciation 5,000 5,000 5,000 5,000

Other Expenses 25,000 38,500 54,500 72,000

EBIT 15,000 22,000 30,000 235,000

Interest 1,000 1,000 1,000 1,000

Earning Before Taxes 14,000 21,000 29,000 234,000

Taxes (40%) 5,600 8,400 11,600 93,600

Earnings After Taxes 8,400 12,600 17,400 140,400

Cash Flow. $13,400 $17,600 $22,400 $145,400

Value of the firm (20%) $67,000 $88,000 $112,000 $727,000

Table II

Balance Sheets

Ending Ending Ending Ending Ending

12/31/00 12/31/01 12/31/02 12/31/03 12/31/04

Cash $ 9,000 $ 41,400 $ 52,000 $ 79,400 $ 4,800

Net Accounts Rec 25,000 15,000 20,000 50,000 305,000

Inventory 35,000 25,000 15,000 10,000 5,000

Fixed Assets 50,000 45,000 40,000 35,000 30,000

Total $119,000 $126,400 $127,000 $174,400 $344,800

Accounts Payable$ 18,000 $ 17,000 $ 5,000 $ 35,000 $ 65,000

LT Debt 10,000 10,000 10,000 10,000 10,000

Common Stock 46,000 46,000 46,000 46,000 46,000

Retained Earnings 45,000 53,400 66,000 83,400 223,800

Total $119,000 $126,400 $127,000 $174,400 $344,800

The Journal of Entrepreneurial Finance & Business Ventures, Vol. 12, Iss. 2

85

Table III

Selected Ratios

Ending Ending Ending Ending Ending

12/31/01 12/31/02 12/31/03 12/31/04

Sales Growth 50.00% 40.00% 114.29%

Gross Profit Margin 50.00% 48.67% 47.62% 72.22%

Net Profit Margin 8.40% 8.40% 8.29% 31.20%

Return on Assets 6.65% 9.92% 9.98% 40.72%

Return on Equity 9.23% 12.68% 15.54% 108.50%

Table IV

Additional Selected Ratios

Ending Ending Ending Ending Ending

12/31/01 12/31/02 12/31/03 12/31/04

Credit Card Expense / Sales 5.00% 5.00% 5.00% 2.89%

Accounts Receivable Turnover 6.67 7.50 4.20 1.48

Days Accounts Receivable Outstanding54.75 48.67 86.90 247.39

Inventory Turnover 2.00 5.13 11.00 25.00

Days for Inventory to turnover 182.50 71.10 33.18 14.60